The rise and rise of passive investing

If there are more passively managed assets than actively managed – what could this mean?

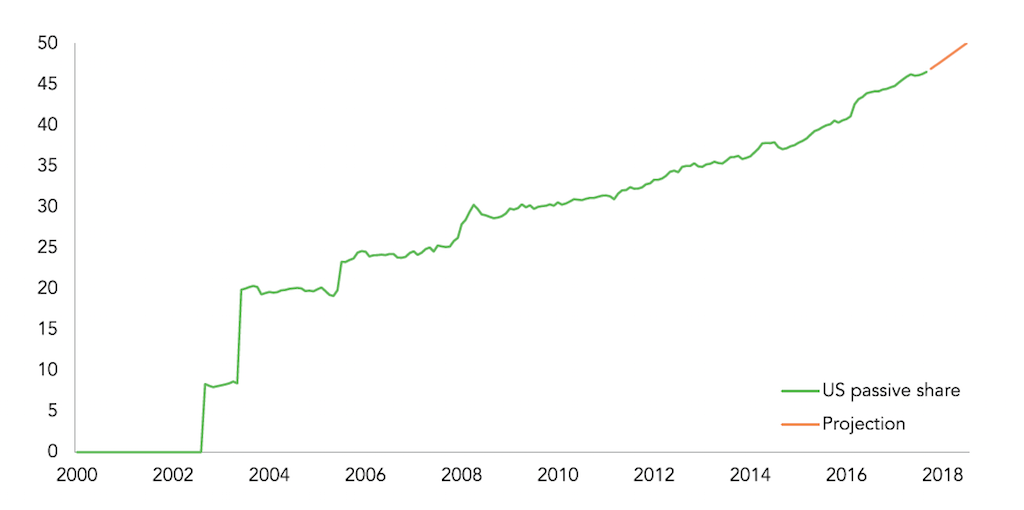

Soon, for the first time ever, there will be more money managed passively than actively in the US. The rest of the world is not far behind.

A cynic might describe passive investing as ‘unthinking’, while adherents might prefer ‘rules-based’ or ‘low-cost’. Regardless, we are crossing a Rubicon. We will politely ignore the irony that every passive investment begins with an active decision as to which index or asset class one would like to passively mimic.

The primary assumption of passive investing is that markets efficiently assimilate all relevant information instantaneously and reflect it in share prices. Effectively, the wisdom of crowds ensures it is near impossible to consistently beat the market, particularly after frictional costs and fees.

What often goes unsaid is that passive investors piggyback off active investors. Their success relies upon active investors constantly assessing and re-pricing risks, with the cumulative ‘best guess’ of all participants accurately and quickly reflected in prices. Active investors’ efforts to capture mispricing are the reason why markets are efficient.

If active investors cease to be rewarded for their efforts by excess returns or management fees then who ensures prices and fundamentals do not diverge? Is there a limit as to how large passives can be before markets

become inefficient?

Furthermore, most indices are market capitalisation weighted, giving larger companies chunkier benchmark weightings.

This has many consequences: passive funds can be surprisingly concentrated around big stocks, and passive investors may find themselves focused in the fully grown, most mature companies.

Most perversely the passive investor is by definition forced to buy the mania – the more overvalued a company, the larger it will be as a proportion of the index.

A stark example of passive investing leading lambs to the slaughter was UK banks exceeding 20% of the index just before the financial crisis. At Ruffer we eschew benchmarks, and this afforded us the flexibility to own no UK banks in the lead up to the crisis, thereby saving our investors from significant losses. Today, it is technology stocks (eg Google and Amazon) which dominate the S&P, and once again we are happy to avoid them.

Duncan MacInnes, Ruffer

If you would like to know more about Ruffer please click the image below

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. The value of overseas investment will be influenced by the rate of exchange. The information contained in this document does not constitute investment advice or research and should not be used as the basis of any investment decision. References to specific securities are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell these securities. Ruffer LLP is authorised and regulated by the Financial Conduct Authority. © Ruffer LLP 2018. 80 Victoria Street, London SW1E 5JL.